Traditional Procurement

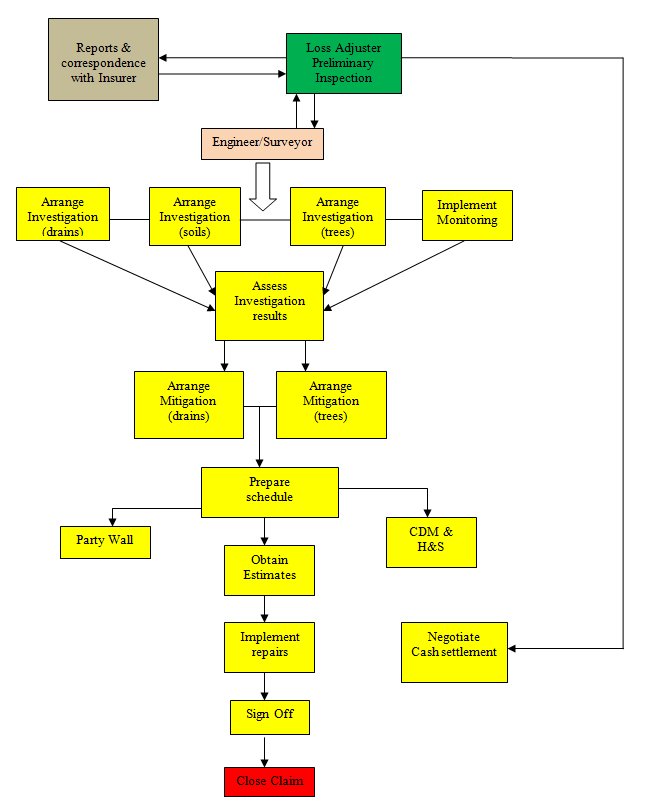

Before the advent of project managed procurement, supply chains and claim handling protocols, a different approach was used. The traditional procurement route places the Loss Adjuster in control of directing the claim but using engineers, surveyors or other specialists as the need is identified. In subsidence cases, it would be normal for an engineer or surveyor to be appointed to deal with monitoring, site investigations, specification writing, contractor selection, tendering and contract administration. Although the project managed route is perhaps more streamlined, the traditional route offers better quality. Not all Insurers want a fast track project managed service and here at Maules we are happy to provide a quality service that utilises the skills of Loss Adjusters, Surveyors and Engineers in their respective specialisms.

Preliminary Inspection

This inspection is carried out so that an accurate report can be sent to your Insurer covering the description and condition of your property, the circumstances relating to discovery of the damage exhibited and recommendations concerning repair. All this information is acquired to enable us to determine liability and confirm to your Insurers the action we propose.

Repudiation Of Claim

In some instances, your claim may not be covered by your policy. The reasons for this are many and varied but if it becomes necessary for us to issue a repudiation on behalf of your Insurer, you will receive a full, written explanation immediately.

There are occasions when your claim is perfectly valid but the repair costs will fall within your policy excess, which means that your Insurer will make no payment.

We would stress that repudiation is not in any way a negative action. By alerting your Insurer to a possible problem you have demonstrated a responsible attitude to the care of your property and from a positive point of view it is far better that subsidence, with its attendant disruption and inconvenience, has been eliminated as the cause of your concerns.

Acceptance Of Claim

When Insurers have received the report following the preliminary inspection, you will receive notification whether or not liability has been accepted. If liability is accepted, the next stage of the process will be put in hand.

On-site Investigations

For subsidence, it is almost certain that more detailed information will be needed. Typically, we will one or two trial holes will be made to expose the house foundations and to assess the nature and condition of the underlying sub soil. It may be necessary to carry out a drain survey and if trees may be involved, obtain an arboricultural report. All the information collected will form part of an engineering report, which will explain in detail the cause of the problem and the measures needed to deal with it.

Mitigation

After the investigations have been completed, it is likely there will be recommendations to carry out some initial measures such as repairing leaking drains or removing nearby trees or other vegetation. After this, monitoring is likely to be needed to see if the building movement has stopped.

Monitoring

Unless the damage is so severe that immediate action is required, your property will be monitored using unobtrusive but accurate measuring devices to confirm if movement is progressive. This is important with regard to remedial action.

Monitoring normally lasts over 12 months to take account of seasonal variations, particularly if trees are a factor. If the damage is slight and seen to be the result of a drainage problem, then the monitoring period after repairing the drain may be reduced to 6 months (depending upon the circumstances).

Stabilisation and Repair

When the investigations and monitoring are complete, any necessary drawings and specifications for final repairs can be prepared based on the technical information that has been gathered. You will normally be sent a copy of the repair proposals for agreement, as will your Insurer. When the specification is agreed, contractors will be invited to tender and the most equitable will be awarded the contract.

Administration

The tender results are notified to your Insurer who will then confirm on which price the work may proceed, you will be advised of this.

The instruction to proceed with the works must be given by you. In contract terms, you become the employer.

Before you commit yourself to any contract for repairs, you should be aware of your financial obligations. Claims are adjusted in accordance with the express terms and conditions of your policy and whilst these vary from Insurer to Insurer, the Loss Adjuster will explain your particular policy provisions and conditions to you.

Once the contractor starts repairs, you will be required to pay your policy excess (if you have not already done so). As the work proceeds, you may decide to off set some or all of the policy excess against certain elements of the work. With your Insurers agreement, cash settlement can be agreed for some of the repairs or in some circumstances, all of the repairs.

When the repairs are finished and have been appropriately certified as being satisfactorily complete, you will be provided with the closing paperwork. The information you receive will vary depending upon the requirements of your Insurer and the scope of our instructions.

Typical Traditional Claim Process

Contact Us

Tel: 01582 602260